CDIC : Insurance for your Canadian Accounts

Finance ·CDIC or the Canadian Deposit Insurance Corporation is a federal Crown corporation that insures your accounts in a financial institution as long as it is a CDIC member. From 17 billion CAD since its creation in 1967, it has gone on to protect 700 billion today.

The CDIC is funded purely by premiums from CDIC members and doesn’t get a dime from your taxes.

You must have seen this logo when you bank with some of the major institutions in Canada.

Just like the padlock in your browser address bar when you browse the web, it gives you a sense of confidence and security as you put away your savings in your bank. But just like that reassuring browser padlock, you may not be fully protected and there is some fine print that you should be aware lest a situation should arise where your bank goes under.

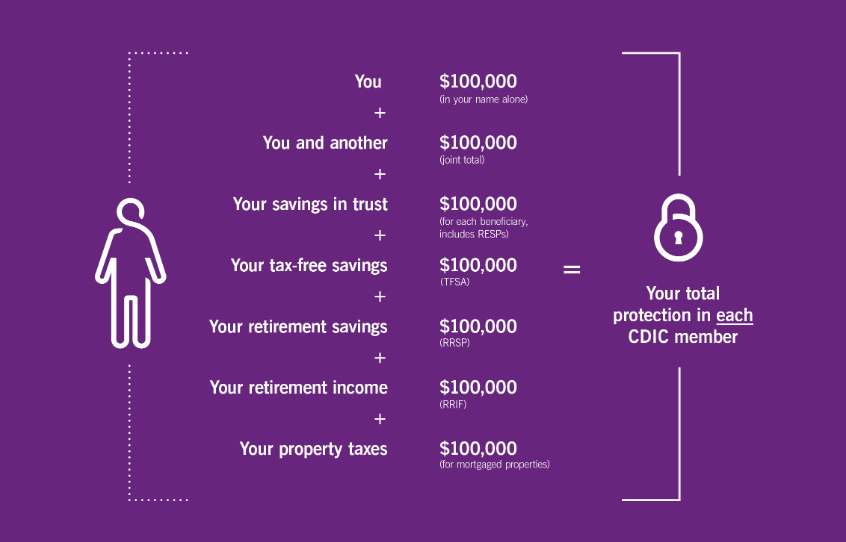

So, what exactly is covered, what is the fine print? This infographic from CDIC explains it in a nutshell:

Each of the 100,000 CAD covered covers checking/savings accounts, GICs and term deposits of 5 years or less.

Notice that it mentions coverage per account is for each CDIC member. So, if Alice has 100k CAD in RRSP savings at TD and wants to contribute more to her RRSP, she is better off opening another RRSP account in RBC to avail an additional 100K CDIC coverage. Same holds true for each of the other account types.

Stocks, bonds, mutual funds and crypto currencies are not covered by CDIC even if they are held in eligible accounts. This is covered by CIPF (covered in a later post).

Edit: US dollars and other foreign currencies were also not covered under CDIC until new rules that came in April 2020. Now, foreign currencies along with CAD are also included in CDIC coverage up to a maximum of 100k CAD.

Expanding a bit more on some of the accounts listed above:

RRSP

Two things to note about RRSP protection:

- Alice has an RRSP and a LIRA (Locked-In Retirement Account which is like an RRSP) at the same bank. Her total coverage for both the RRSP and LIRA is 100,000 CAD since they are both considered retirement savings.

- Spousal RRSPs coverage is based on the owner irrespective of who contributed to it. So, if Alice contributed 50,000 CAD to her husband Bob’s RRSP to bring it a total of 130,000 CAD, only 100,000 CAD of that is covered since the RRSP coverage per account holder is 100k.

RESP

RESP coverage of 100,000 CAD is per beneficiary. So if you open an RESP for each of your kids, they are individually covered up to 100k.

Joint Accounts

If Alice and Bob opened a joint account at TD, that account would be covered up to 100k irrespective of the number of owners. And this coverage is outside of each owner’s individual account coverage. If you wish to read more about how the deposit insurance coverage works, here is the CDIC page for the same.

When a bank fails

When a CDIC member goes under, a process called resolution is undertaken by the CDIC, where the institution is restructured or closed and eligible deposits are repaid. You can take comfort in the fact that since CDIC’s creation, it has handled 43 failures (the last one in ’96) and every single dollar under CDIC protection has been repaid. Strangely, there was not a single failure of a CDIC member in 2008 -2009 financial crisis, probably because Canada did a good job weathering that crisis.

CDIC Tools:

- Want to know if your bank a CDIC member? Here’s a full list of CDIC members.

- CDIC also offers you a handy calculator if you wish to see how much of your deposits are covered.

And if everything I mentioned above went over your head, allow this suave dapper guy give an overview of how CDIC works.

Liked this post? Share them lest others should find this useful.